In 2025, NagaCorp appointed Political & Economic Risk Consultancy, Ltd. (PERC), an independent third party from the Company, to conduct a research and review on investment risks in Cambodia. Established in 1976, PERC is headquartered in Hong Kong and engaged principally in the monitoring and auditing of country risks in Asia. From this base, PERC manages a team of researchers and analysts in the ASEAN countries, the Greater China region, and South Korea. Corporations and financial institutions use PERC's services to assess key trends and critical issues shaping the region, identify growth opportunities, and develop effective strategies for capitalising on these opportunities.

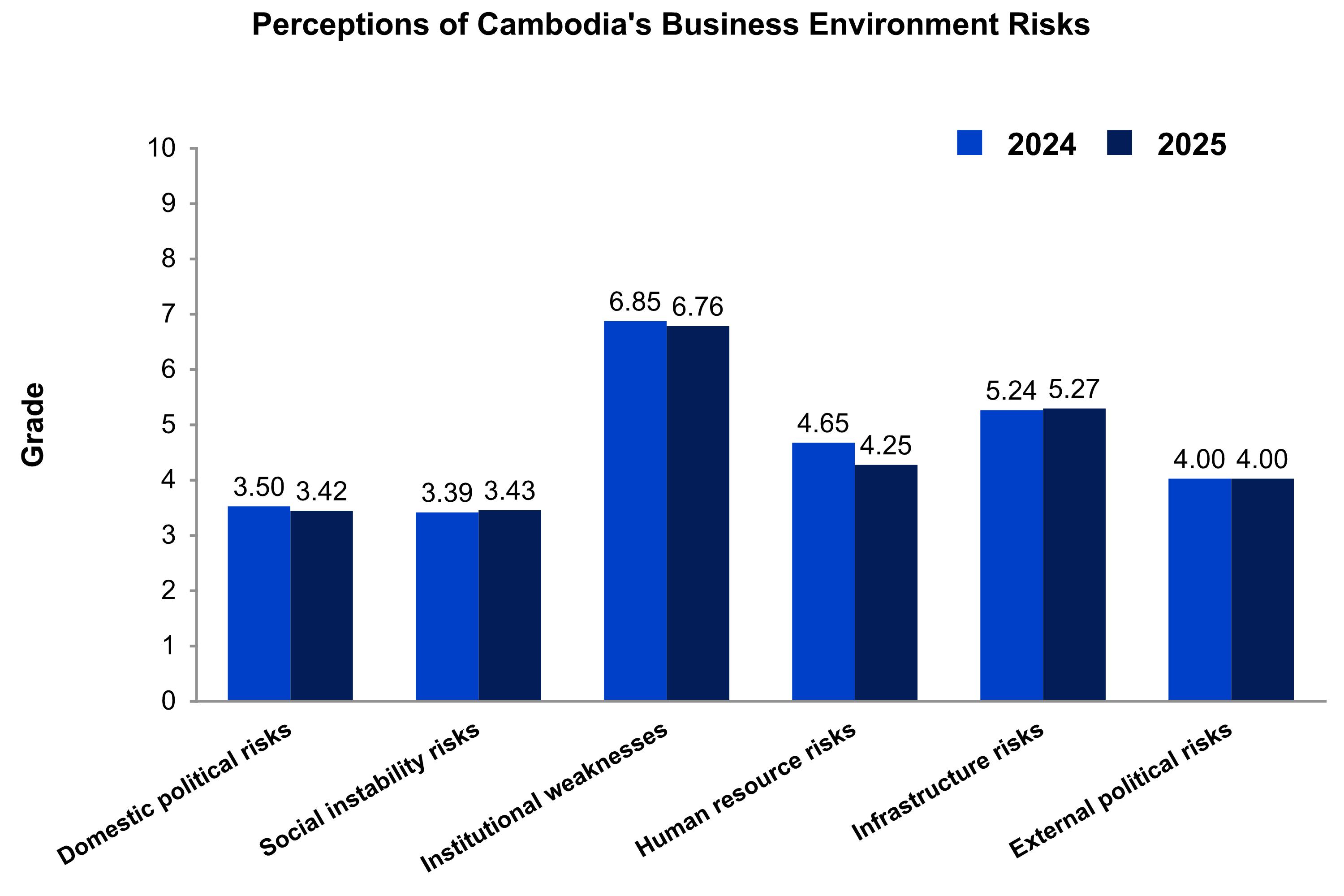

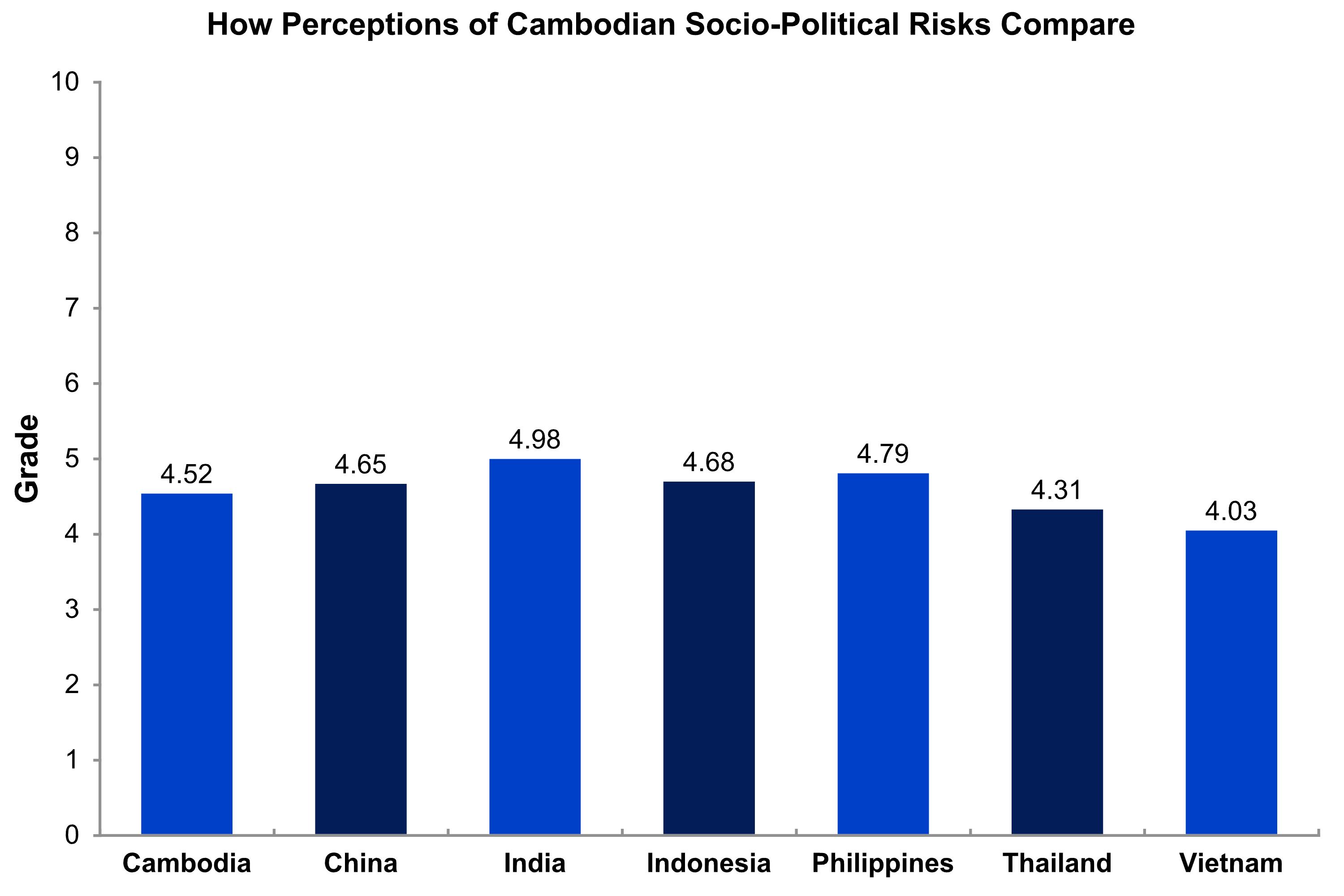

PERC has assessed and reviewed Cambodia’s political, social, investment, and macroeconomic risks related to NagaCorp’s casino, hotel, and entertainment business operations. In arriving at the findings below, PERC has taken into account, amongst others, domestic political risks, social instability risks, institutional weaknesses, human resource risks, infrastructure risks, and external political risks.

Based on the assessments and reviews carried out between end-November 2025 and the end of December 2025, PERC summarised the findings below:

Grades range from zero to 10, with zero being the best grade possible and 10 the worst.

PERC quantities investment risks in Cambodia through the measure of the following variables:

- Domestic political risks

- Social instability risks

- Institutional weaknesses

- Human resource risks

- Infrastructure risks

- External political risks

Each variable comprises several sub-variables relating to specific aspects of the assessed category. The weighted sum of the grades for sub-variables equals the score of a broader variable, while the weighted sum of the grades of the broad variables defines overall investment risks in Cambodia. PERC has treated each variable as having equal importance or weight.

Summary

The past year has been challenging for Cambodia economically, but politically the country demonstrated its stability and the competence of its leadership to deal with problems. Having already orchestrated a smooth political transition in 2024, the government was able to deal with difficult external issues that lasted throughout 2025 and still maintain a rate of economic growth in excess of 4%-5%, which was in line with other ASEAN nations. It did so by sustaining export growth, keeping the exchange rate steady and inflation low, attracting a record amount of foreign direct investment, and demonstrating fiscal responsibility by restraining expenditures to compensate for lower revenues.

The economic development that was most relevant to NagaCorp’s business environment was the weakness in foreign tourism inflows in the second half of 2025 that reversed a recovery that was evident in the first semester. However, the negative nationwide numbers exaggerated the deterioration, since they were overwhelmingly due to a plunge in visitors from Thailand who normally travelled to Cambodia by land routes. Those inflows were seriously disrupted from July onwards by border skirmishes involving the Thai and Cambodian militaries. The chances are high that the conflict will be ended shortly and that visitors by land will resume in 2026, but the much bigger reason for optimism is that the border conflict had no impact on foreign visitor inflows by air to Phnom Penh, the capital and location of NagaCorp's main operations. Such inflows increased by more than one fifth and should keep growing in 2026 considering that a new international airport has just opened with a bigger capacity, more direct air routes have been opened to a wider range of cities in China and elsewhere, and there will be at least a four-month period from mid-June until mid-October when visitors from China, Hong Kong, and Macau will be able to visit Cambodia without obtaining a visa.

Cambodia faces more uncertainties that could keep the economy limited to a GDP growth of 4%-5% in 2026, but as these factors are resolved, growth could accelerate to above 5% in 2027. The main risks include more disruptions to Cambodian exports caused by abrupt changes in US tariff and trade policies, continued weakness in the local residential real estate market due to a lack of foreign-buyer interest, and exaggerated foreign perceptions of personal security risks in Cambodia that will take time to rectify.

On the other hand, foreign direct investment inflows should remain strong. Economic growth will be underpinned by continued heavy spending on roads and other infrastructure projects. The agricultural sector will act as a buffer for the economy and grow in importance due to the increase in local processing of foodstuffs for export.

Of all the major categories of sociopolitical risks, external risks have risen the most in the past year. Of Cambodia’s other socio-political risks, the highest relate to institutional weakness, physical infrastructure deficiencies, and human resource limitations.

External developments made it harder for the government to reach its economic goals. However, other variables used to define domestic political risks improved, keeping this category low. Social instability risks were also low, despite the unexpected return of workers from Thailand.

Cambodia’s new government has also had success in strengthening the Kingdom’s relations with other major foreign governments, except for Thailand. US-Cambodian relations have improved substantially over the past year and are still moving in a favourable direction, despite the disruptive tariff policies of the Trump Administration. Prime Minister Hun Manet has personally cultivated closer relations with the leaders of Japan and South Korea, even as he has maintained Cambodia’s extremely close relationship with Mainland China. The gains on the broad foreign policy front should pay favourable economic dividends for Cambodia in 2026 and following years.

Positive Developments

- Cambodia’s long-term growth outlook is good. To be sure, there will be ups and downs, but the long-term prospects are positive due to demographics (young), policies (pro-business), and political stability.

- Cambodia maintained strong relations with China over the past year, while it has improved relations with other countries like the US and Japan, which should help to stabilise the geopolitical environment, reduce trade and investment risks, and improve its capabilities for dealing with problems like criminal cyber scam networks.

- The increase in US tariffs and the slower-than-expected recovery in China that contributed to the slowdown in Cambodia’s economy in 2025 and contributed to uncertainty are likely to subside as issues in 2026. Cambodia’s exports to the US continue to grow despite the higher tariffs, while China’s economy has stabilised in ways that will encourage more outward investment growth and foreign travel by Mainland tourists. Cambodia should benefit from these trends.

- Reforms undertaken in the past year include streamlining and reducing import licensing and regulatory requirements, enhancing intellectual property protection, and reducing Cambodia’s tariff and non-tariff import barriers. These reforms should help ensure that the inflow of foreign direct investment remains strong.

The Challenges

- The most formidable long-term challenges Cambodia faces involve the need to strengthen key institutions like the education system, legal system, judiciary, and tax system. The main short-term challenges include dealing with a correction in the residential real estate sector, ending the border conflict with Thailand, and cracking down on activities by organised crime that have hurt perceptions of personal security.

- There is concern over financial sector problems due to the property market downturn, sluggish credit growth to the private sector, and rise in the level of non-performing loans.

- Border problems with Thailand have sparked return migration, which is an added burden on the economy in the short term due to the need to find work for those returning to the country and the cutoff in their remittances from Thailand. The conflict has also exaggerated perceptions of security risks to foreign tourists that need to be countered quickly.

- Cambodia’s dependence on the US as a market is still growing and exports are vulnerable to periodic major disruptions. There is also still a risk that the US might impose higher tariffs or other restrictions on components sourced by Cambodian factories from suppliers in Mainland China that are used to produced goods ultimately destined for the US market.